“The Federal Open Market Committee (FOMC) has considerable control over short-term rates. We have much less influence over long-term rates, which are set in the marketplace.” – Jerome Powell, Federal Reserve Chairman.

It’s been almost three years since the Federal Reserve embarked on its journey of increasing interest rates. The post financial crisis era of easy money was finally coming to an end. We remember predictions of bond market carnage amid the rising rate narrative.

We were curious how the popular consensus of the bond apocalypse lined up with reality. What we found was surprising (even to us).

Since 2015, every bond asset class has had a positive annualized return despite the Fed hiking interest rates seven times.

We touched on why this phenomena isn’t unprecedented in our previous post, “What Actually Happens During a Fed Hike Cycle” (2016).

We attribute the large gap between perception and reality to the following:

- Bonds are complex, confusing, and boring.

- Bond yields have gone down in the U.S. (until recently) for 30+ years.

- The Fed is literally telegraphing its every move and some investors haven’t adjusted to the new normal.

- Fear sells (financial media & Wall Street have spun the tale of bond demise for years).

We bring this up now because the Fed is set to hike for the eighth time in September, but we’re seeing the same tired stories:

Nasdaq: “Now is the Time for Floating Rate Bonds” (9/06/2018)

Bloomberg: “Bond Traders Dash for Cash as Fed Hike Odds Soar” (9/12/2018)

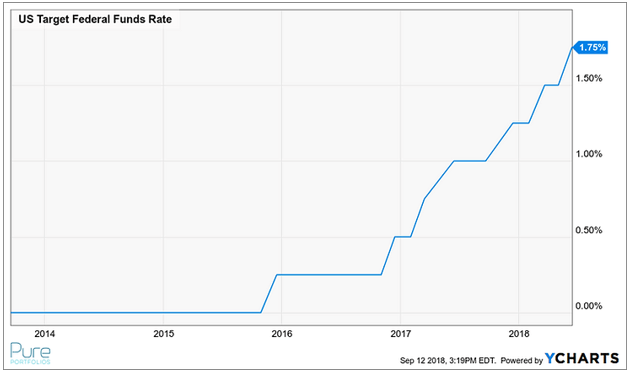

Source: YCharts

The Fed has methodically increased interest rates the last three years. It’s an art to balance market expectations and monetary policy.

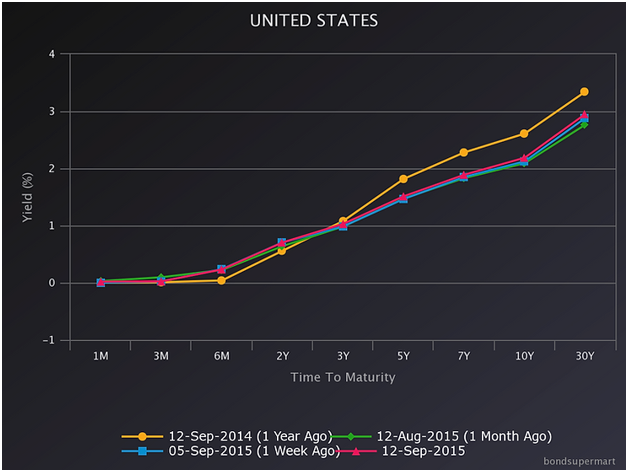

Source: Bondsupermart.com

The above graphic shows the yield curve in the fall of 2015. Notice the upward slope as short-term yields (1 – 6 month maturities) were virtually zero. Longer-dated maturities (10 & 30 year bonds) were hovering around 3%.

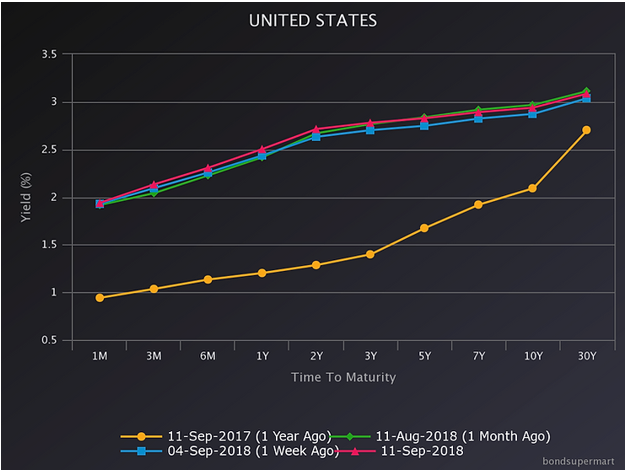

Source: Bondsupermart.com

Fast forward to September 2018. Short-term yields across the curve are meaningfully higher. Longer-term bond yields remain stuck in neutral. Our opening quote by Fed Chairman Jerome Powell sums up this quandary perfectly, the Fed has no control over long-term bond yields.

Despite rising interest rates, bond returns across the board have held up well. We ran performance for major bond asset classes from January 2015 to August 2018:

CAGR = Compounded Annual Growth Rate (Annualized Return)

StDev = Standard Deviation measures the dispersion of returns vs. an average value. The larger the percentage, the wider dispersion of returns.

Source: Portfoliovisualizer.com

The above table shows returns across short, intermediate, and long-term U.S. Treasuries.

Source: Portfoliovisualizer.com

The above table shows returns across short, intermediate, and long-term investment grade corporate bonds.

Source: Portfoliovisualizer.com

The above table shows returns across the total U.S. bond market (aggregate index), high-yield/junk, and global bonds.

A few things stick out:

- Returns were positive across all bond asset classes.

- Short-term bonds performed worse than long-term bonds. Most money managers were pounding the table to own short-term bonds as rates rose — we railed against this approach in the past (See “Mismanaged Bond Portfolios Are Costly“).

- Owning a mix of different maturities and styles smoothed out returns and risk.

- Higher short-term interest rates does not necessarily mean bonds post negative returns.