“Should any political party attempt to abolish social security, unemployment insurance, and eliminate labor laws and farm programs, you would not hear of that party again in our political history.” – Dwight D. Eisenhower, November 8, 1954

According to the Pew Research Center, 10,000 baby boomers retire every day. Many are asking the same question…

When should I take my Social Security benefits?

There’s no shortage of content on the subject. A simple Google search reveals almost a billion hits. Opinions range from taking benefits ASAP to deferring until age 70.

Within your social circle, your neighbors will share their “foolproof” strategy to maximizing benefits. Your brother’s wife’s cousin will offer “one size fits all” advice to anyone with a pulse. Chances are your great Aunt Bertha also has a strong opinion on the subject.

The decision when to take Social Security is a big one, but it shouldn’t be made in a vacuum, rather in the context of a holistic plan.

Here’s how our newly retired friends, Cecil & Bertha, might approach the Social Security equation:

Set up an online account through the Social Security website

Track your earnings history and see an estimate of benefits by age. We find this useful for those still working to ensure work history & income is correctly entered. You can even use the info for pre-retirement cash-flow planning.

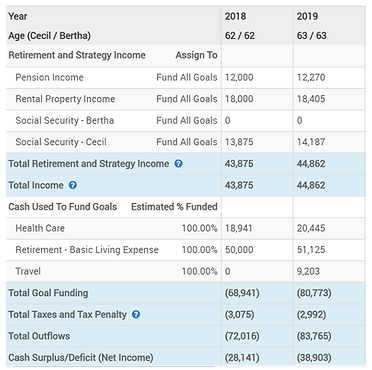

Start modeling Social Security benefits alongside other retirement income, expenses, and taxes

Source: MoneyGuide Pro

The decision when to take benefits will become more clear in the context of household cash flows.

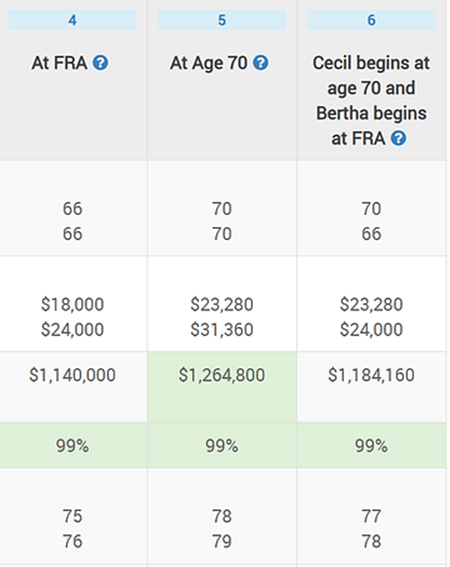

Run different Social Security strategies relative to your plan

Source: MoneyGuide Pro

Once we have our cash flows set, we can begin to model alternative Social Security strategies. In this case, the maximum lifetime benefit has Cecil and Bertha taking benefits at age 70. However, the 99% probability of success shows their overall plan will be successful regardless of what age they realize Social Security benefits. Finally, the ages at the bottom show how long Cecil and Bertha must live to “breakeven” as a result of deferring Social Security (as opposed to taking benefits at age 62).

Explore spousal options if married

Some spousal strategies include: benefits for a non-working spouse, file and suspend, working 35 years, deferring benefits until 70.

The nuances of the Social Security program are complex and fluid. When in doubt, check with the folks at the Social Security Administration office. We have heard they are a great resource for questions.

Embrace uncertainty

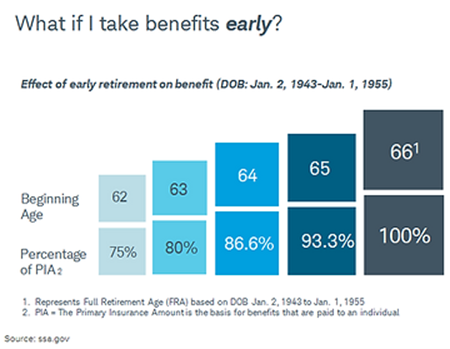

We can only make decisions based on the information we have today. The biggest unknown is life expectancy. If you have health problems or shorter life expectancy in your family history, it might makes sense to take benefits sooner. If you’re in good health and expect to live longer, it might make sense to wait.

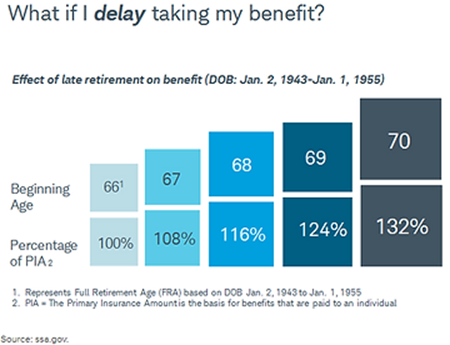

Generally speaking, erring on the side of deferring is beneficial. The guaranteed increase of benefits lasts a lifetime and is not subject to market risk. If you’re worried about outliving your investable assets, and/or financial market risk, locking in a higher lifetime benefit sounds pretty good.

Evidence-Based Investors make decisions based upon accurate inputs, objective data, and disciplined rules. When to take Social Security benefits should be in the context of a robust financial plan, not in isolation. Strip out the emotion, misinformation, and what your Aunt Bertha did in 1985 to make the best decision for you.

Our favorite Social Security Resources:

AARP Social Security Resources

Social Security Administration