“My investment plan was built with the assumption that I would experience a number of both bull and bear markets over the years.” – Ben Carlson, author of A Wealth of Common-Sense blog

I’ve seen competitors sell one year of outstanding performance.

I’ve seen mutual fund companies run commercials touting their latest five-star fund.

I’ve seen a prospective client collect performance data for five different advisors. The plan was to hire the advisor with the best numbers in the previous two years.

I don’t know how every situation ended, but there’s a reason the SEC mandates the disclosure “past performance is not a guarantee of future results.”

To be fair, we cannot dismiss past performance (especially over the long-term), but the question remains…

How much should we value past performance when making investment decisions?

The good news is we have a trove of data tracking how the top performing mutual fund managers do in the subsequent years.

It’s not pretty.

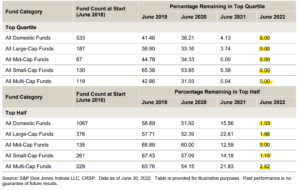

The above chart shows top performing mutual funds by equity style in June 2018 (left column). The following columns show the percentage of funds remaining in the top quartile (top graphic) and percentage of funds remaining in the top half (bottom graphic). Out of the 533 top performing funds in June 2018, none were in the top quartile in June 2022!

It seems the best performing managers, funds, strategies, styles, and advisors find it virtually impossible to replicate outstanding performance in subsequent years.

Did these smart people suddenly turn stupid?

Nope.

Investment styles go in and out of favor.

Luck has a huge impact on short-term investment returns (< 10 years). Skill wins out over the long-term (10+ years).

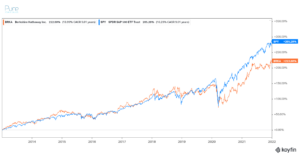

Warren Buffett trailed the S&P 500 from 2013 to 2021. Many pundits said he had lost his golden touch. It turns out, Mr. Buffett’s bread and butter value style of investing was out of favor vs. high flying technology companies.

Source: Koyfin

The above graph shows Warren Buffett’s Berkshire Hathaway (orange) cumulative return vs. the S&P 500 (blue, 1/2013 – 12/2021). Mr. Buffett trailed the S&P 500 for the better part of a decade. While many proclaimed Mr. Buffett’s time had passed, it turns out that growth was in favor while value investing was out of favor.

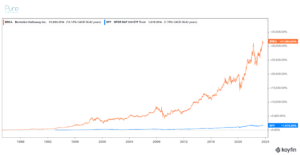

Zooming out, it’s not hard to see why so many regard Warren Buffett as the greatest investor of all-time…

Source: Koyfin

The above graph shows Warren Buffett’s Berkshire Hathaway (orange) cumulative return vs. the S&P 500 (blue, 1985 – 9/2023). Despite periods of inevitable underperformance, Mr. Buffett’s skill over the long-term is matched by few.

What can we learn about past performance and future allocation/investment decisions?

- The best performing funds, advisors, strategies, etc. often find it difficult to sustain exceptional performance.

- Investors that chase today’s best performing areas of the market usually end up getting burned (hence, past performance does not guarantee future results).

- Luck can explain short-term performance results. Skill can explain long-term performance results.

- Investment styles go in and out of favor. An investor with incredible results during one period isn’t a genius. The same investor that posts horrible results the following period isn’t an idiot.

- Investors that obsess over performance, but don’t pay attention to how much risk they are taking could be setting themselves up for failure (see “Is Your Portfolio Drunk or Sober?)”.

Most importantly, good investing isn’t trying to earn the highest return possible. Good investing shouldn’t be exciting. In my opinion, good investing is earning reasonable returns consistently over time.