“Predicting what the world will look like fifty years from now is impossible. But predicting that people will still respond to greed, fear, opportunity, exploitation, risk, uncertainty, tribal affiliations, and social persuasion in the same way is a bet I’d take.” – Morgan Housel, author of Same as Ever

Resurgent inflation

Federal Reserve gaffe

Delusional expectations for frothy technology & AI stocks

Poor investments and breakdown in corporate earnings

Geopolitical risk

Trade war

U.S. government debt burden & deficits

These are potential land mines that could derail the current bull market.

We can get ahead by understanding when it comes to investing, difficulty is a guarantee. The doubt. The raw emotion. The daily flow of information coming at us. The confusion. The ugly loss. They will come. You don’t get to choose whether they appear, or when, but you do get to choose how you prepare and respond.

The truth is no one knows what the source of the next crisis will be. Nor do we know the timing of such an event. However, we can set our watch to how humans react.

In our opinion, the humble investor can take advantage where others become too emotional, too confident, too complacent, and too exposed to today’s investment themes.

The biggest mistake humans make, from Wall Street professionals to retail investors, is pretending we can predict the future in the first place. Playing the prediction game is an automatic disadvantage because we are relying on a framework that doesn’t work. Making gut calls, relying on our narrow personal experiences to explain how the world works, or seeking opinions that validate our own is a recipe for disaster. Unfortunately, this is how many investors make allocation decisions.

Market disruptions are a function of consensus predictions about the future and what actually happens. In other words, the gap between what we think will happen and what actually happens is wider than we think. The world is much more random, unpredictable, and full of surprises than we care to admit.

A better approach is to lean into history, keep an open mind, be able to change one’s mind, and view the world with a healthy amount of humility.

Accepting the occasional loss is an underrated skill in investing. We’ve seen more money lost by trying to get out of the way of every market dip. This behavior is unanchored from reality.

Here are some other ways investor’s end up on the wrong side…

- Take too much risk during good times. People make stupid decisions when things are going well. The seeds to next crisis are almost always sown during prosperous times (“Stability Breeds Instability“).

- Believing current market conditions will last forever. Humans anchor to recent history to make predictions about what comes next (recency bias). An investor exhibiting recency bias would proclaim good markets will last forever or there’s no end in sight during a difficult market (The Danger of Recency Bias).

- Playing the prediction game. Humans love certainty and control, which is why we entertain forecasts even though we probably know better.

- Making allocation decisions based on daily news flow. If it’s on the front page of the newspaper, the market has priced it in. If your neighbor is talking about it, it’s less risky than you think. True risk is what’s left over after you’ve thought of everything (The Dog That Didn’t Bark).

- Chasing today’s winners. For example, most prospective client portfolios we review are massively overweight U.S. technology stocks. Many have unreasonable expectations about future returns and no clue how much risk they’re taking.

As a humble investor, this is what we can do instead…

Be very intentional about where and why you’re taking risk. Know what you own and how it benefits your portfolio. One recurring error we see is owning 15 different mutual funds across 7 different investment managers. It’s impossible to understand what you own, let alone how much risk you are taking.

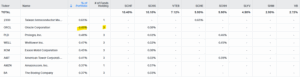

We can help unpack what prospective clients own by our exposure matrix…

Source: Koyfin

The above graphic shows how much Oracle stock the example prospect owns across accounts and funds. In this case, Oracle is 0.49% of the portfolio which is held across three fund holdings. This is a great way to pull back the curtain on risk. It’s fine to take known risks, however, unknown or unintended risks are what we want to avoid.

Have an umbrella before it rains. Many investors pile into risky corners of the market during good times, they try to jump out of the way when the cycle turns negative. This is a horrendous way to invest. A better approach is to build a portfolio that reflects your risk profile and build a non-emotional framework for making decisions.

Shun forecasts and predictions. Engage with history. Spend less time clicking buttons online. There’s no excess return or insight on the front page of the newspaper.

Be honest with yourself. Have you made past emotional decisions? Did you react poorly to the last market pullback? In our opinion, bear market feedback is gold (unfortunately, many investors repeat the same mistakes).

Don’t let a crisis go to waste. There are few fat pitches in investing, putting capital to work in a difficult market is one of them. Poor years are often a precursor to good years. Purchasing pessimism (as reflected in low prices) can pay off on long horizons.

The humble investor understands difficult markets and the occasional loss are part of investing. The humble investor shuns forecasts and predictions, instead relying on history to frame potential outcomes. The humble investor understands where the risk is in their portfolio (intentional risk) and has a formulaic plan to make decisions during a market selloff. The humble investor will be honest about their shortcomings and blind spots, learning from past behavior to make better decisions going forward. The humble investor will deploy idle cash during market selloffs understanding putting capital to work when others are panicking is the closest thing to an investment “fat pitch”.

Dan Rasmussen, author of the “The Humble Investor,” said it best…

“Human psychology is the one great constant in investing. Interest rates go up and down, stock markets boom and bust, but human psychology never changes. And I believe that studying how people think about and react to markets—and particularly studying the most common mistakes investors make—can give us an edge in a surprising world.”

If you want to learn more about Pure Portfolios’ non-emotional investment approach, shoot us a note insight@pureportfolios.com. Many of our clients are former do-it-yourself investors and clients working with expensive, conflicted Wall Street advisors.