“Remember how excited people were about bonds when rates were under 1%? You see how bearish people are about bonds today, with yields at 4.5?” – Jared Dillion, author & investor

Bonds have had a historically bad run. If you’re looking for the source of performance drag in a diversified portfolio, bonds are the most likely culprit.

It turns out, higher unexpected inflation and an aggressive Fed rate hiking campaign are bad for most every asset class, but especially bonds.

I don’t think you can underestimate the psychological shock for the average investor. Bonds were thought to be safe, but in some cases are down more than “riskier” stocks.

Why would anyone own such a confusing and down in the dump’s asset class?

Fair question, it hasn’t been pretty…

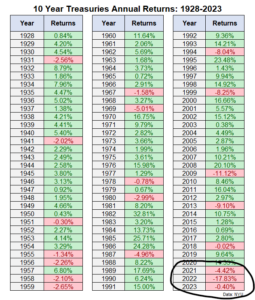

Source: NYU, Ben Carlson

The above graph shows 10-year Treasury annual returns (1928 – 2023). 2022 marks the worst total return -17.83% for the 10-year in history. If 2023 posts a negative return, that would mark three consecutive years of losses, which would be the first over the last 95 years.

The pain hasn’t been limited to 10-year U.S. Treasuries. The majority of bond asset classes have posted negative 3-year annualized returns (red)…

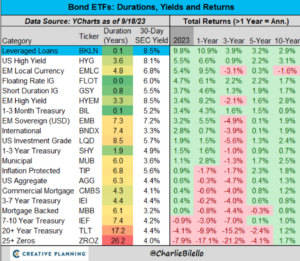

Source: Creative Planning, Charlie Bilello

The above graphic shows bond ETF returns by duration (maturity), yield, and total returns. The 3-year annualized numbers leave much to be desired for bond investors. The longer the maturity term, the more pain. The 20+ year Treasury ETF experienced a -15.2% loss every year for the last three years!

The carnage in the bond market was the perfect storm.

Starting record low interest rates & bond yields + highest unexpected inflation in ~40 years + aggressive Fed hiking campaign = historical losses for bond investors.

However, it’s not all bad…

Starting Yield & Future Returns

While future equity returns are darn near impossible to predict, starting bond yields can potentially “explain” future returns.

Historically, the higher the starting yield, the better future returns for bonds.

Source: Bloomberg

The above graph shows there’s a strong correlation between starting 10-year Treasury yield and future bond returns (Bloomberg US Aggregate Bond Index, 1976 – 2021). For example, in the 2000’s, the 10-year U.S. Treasury was yielding 6.7%. The following decade the Bloomberg US Aggregate Bond Index posted a 6.3% return per year.

Vanguard has published similar research showing higher starting yields’ relationship to higher future bond returns…

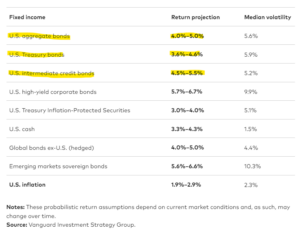

Source: Vanguard Investment Strategy Group

The above graphic from Vanguard shows projected future returns for the U.S. bond market, U.S. Treasuries, and U.S. corporates between 3.6% – 5.5% per year over the next 10 years. These figures are for investment grade issues i.e. high quality bonds. A big component of the rosy return profile for bonds is higher interest income.

The Fed Cycle and Potential Rate Cuts

When interest rates go up, that’s usually bad for bonds (especially for longer maturity bonds). An investor would be locked in at lower rates, missing out on the new higher market rate.

Lower interest rates are good for bonds. An investor would receive higher than market interest, while the value of the bond potentially goes up.

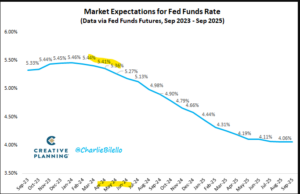

The Fed futures market is pricing in interest rate cuts in spring 2024 (these projections can change) …

Source: Creative Planning, Charlie Bilello

The above chart shows market expectations for the Fed funds rate. The market is saying the Fed is *almost* finished with interest rate increases. After a 3-5 month pause, the Fed is expected to cut rates starting in early 2024. Historically, rate cuts are a tailwind to bond investors.

What can we learn from the last three years of bond market pain?

- Unexpected inflation is bad for bonds (and most other asset classes).

- Aggressive interest rate increase campaigns are bad for bonds, especially longer-term maturities.

- Bonds have been a major drag on diversified portfolio returns.

- People associate value investing with stocks, but it can apply to bonds too (hat tip Jared Dillion).

- Looking forward, one could argue the prospect for bonds are more attractive than they’ve been for 10+ years.

- Higher rates & bond yields are bad for borrowers, but good for savers & investors.

For more reading on bond investing…

“Juicy Money Market Yield Won’t Last”