“Investors are always searching for good ideas, when what they need are good habits.” – Jason Zweig, Wall Street Journal & author

If you asked the average person what a financial advisor does, you might hear something like, “researching which stocks to buy,” or “trying to find the next winner in the stock market.”

While most good advisors do spend a chunk of time building out their investment framework, investing new money, rebalancing, etc., gone are the days of your advisor picking up the phone and suggesting a client “buy 1,000 shares of XYZ Corp. because word on the street it’s gonna move up when they report earnings.”

Empirical data shows this isn’t a good way of investing and picking individual stocks is really hard. Even the best and brightest that pick stocks for a living aren’t any good at it (the SPIVA report tracks how many active managers beat their benchmark. The answer? Very few).

If investing is not the most valuable service an advisor provides, what is?

A prospective client asked me what they would get for our fee. At the top of the list, I always lead with behavioral coaching.

The prospective client cut me off mid-sentence. What the heck is behavioral coaching?

In simple terms, behavioral coaching is a framework for making better financial decisions.

Money is emotional. We all have philosophies on money. Some of our money ideas come from personal experience. Others originate from what our parents preached. Some of us scour the internet for how to get ahead financially.

Furthermore, when it comes to your own wealth, only one person understands the blood, sweat, and tears that went into building your nest egg…you.

Add it up and we have accumulated an identity that shapes our attitude on money, risk, and investing (I share mine here, see “How I’m Personally Invested“). It also comes with biases, blind spots, and emotions that could be a detriment to reaching our financial utopia.

How valuable is behavioral coaching in an advisor/client relationship?

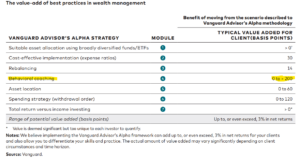

It’s an inexact science, our friends at Vanguard gave it a shot…

Source: Vanguard

The above graphic shows the typical value add for an advisor in basis points (100 basis points = 1%). According to Vanguard, behavioral coaching could potentially add up to 200 basis points or 2% to an investor’s return simply by making better money decisions. Notice the other value add activities have nothing to do with market predictions, stock picking, allocating to exotic private equity, etc. All the value-add activities involve optimizing the things right in front of us.

In my opinion, behavioral coaching is more important than ever.

Pre-internet, it took effort to get information. You had to buy a newspaper or drive to the library. There was friction.

The friction has been removed with the emergence of smart phones, 24/7 media coverage, and social media.

We wake up and our iPhone is pinging with market news, stock price movements, and attention-grabbing headlines (scary headlines sell more ads, see “Retirement Propaganda War“).

One might think the more information we have, the better financial decisions we can make.

It’s the opposite.

According to Slate, there is evidence to suggest those that consume financial media make worse financial decisions than someone who doesn’t (the article mentions CNBC, it could be any financial program).

The issue is that 99% of what you read or hear can be nonsense. It’s easy to take a random headline or idea and apply it to our own circumstance with zero understanding of context, conflicts, or incentives behind the scenes.

I’ve seen this is practice. There is a huge increase in my time spent debunking conspiracy theories, doomsday YouTube videos, and sensationalized articles.

Remember 2023 when everyone was talking about the dethroning of the U.S. Dollar? Darn near every meeting from January to May 2023 I was asked about it (see my blog response, “The Demise of King Dollar“). Fast forward less than a year later, the U.S. dollar has never been more dominant, counting for the largest share of global trade ever. How ridiculous was all the hype in hindsight?

Back to behavioral coaching, what does it look like in practice?

It starts with building a foundational financial plan. This might sound daunting, but it’s capturing income, expenses, social security info, taxes, gifting, travel, cost of healthcare, other goals, etc.

Once we have our base plan, we can use it to run scenarios. I call it a personal decision center.

Rather than take a wild guess on how a money decision impacts our plan, we can run the numbers. Here are some common examples…

- Can we buy a second home?

- If we sell our house to downsize, how much house can we afford?

- Should we pay off the house or invest the money?

- Should we do a Roth conversion?

- What age to take Social Security?

Money is emotional. We understand. By having a non-emotional decision center, a good advisor can help people make objective, data backed decisions.

Ben Carlson of the Wealth of Common Sense blog said it nicely…

“The best financial advisors don’t just tell you what to do; they give you a better decision-making framework to make good choices over and over again.”

That’s an advisor’s true value.

Want to learn more about how Pure Portfolios works with clients? Shoot us a note at insight@pureportfolios.com